In a strategic move poised to reshape the financial landscape of the United Kingdom, Affirm, the renowned American buy now, pay later (BNPL) firm, officially launched its services in the UK on Monday. This expansion marks Affirm’s first foray beyond North America, signaling a growing interest in the international market and an ambitious agenda to tap into the UK’s lucrative consumer finance sector.

Here's ads banner inside a post

A Growing Demand in the UK Market

Founded in 2012, Affirm has become synonymous with flexible payment solutions, allowing consumers to make purchases and pay for them over time. Max Levchin, Affirm’s CEO, highlighted the burgeoning demand from merchants in the UK as a significant factor in their decision to expand. “It is a huge market, it’s English-speaking,” Levchin noted in a recent interview, emphasizing the suitability of the UK for Affirm’s model.

Here's ads banner inside a post

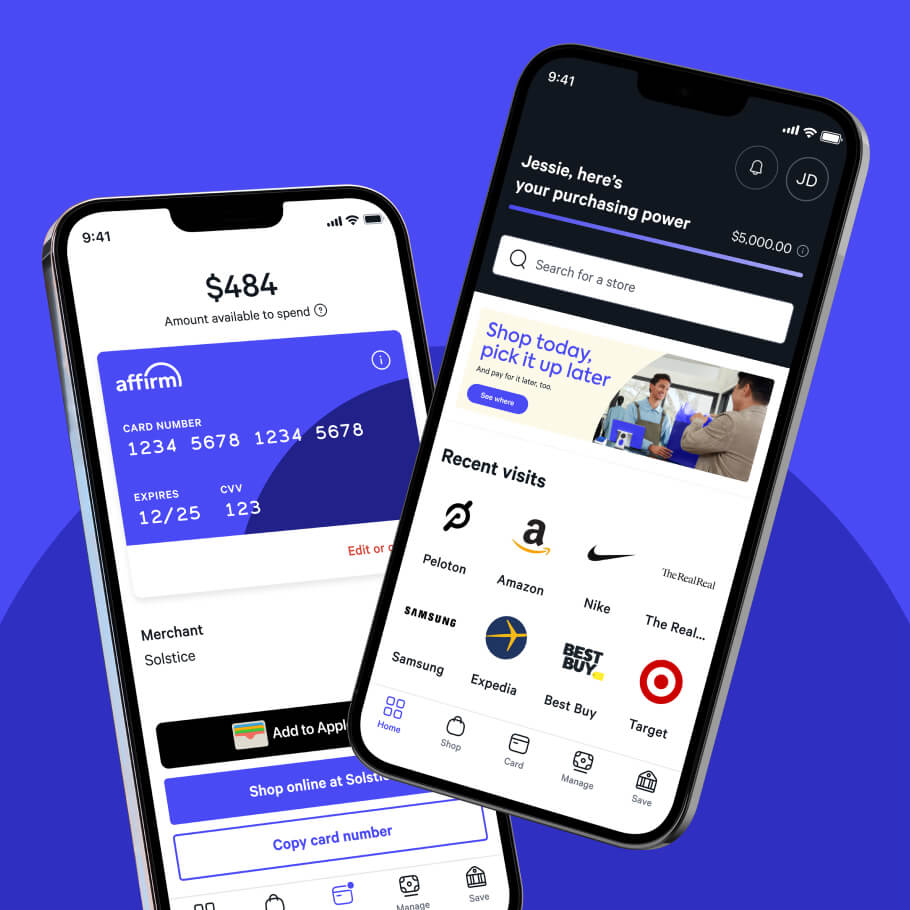

With over 50 million users globally and partnerships with more than 300,000 active merchants, including major players like Amazon, Shopify, and Walmart, Affirm’s expansion is anticipated to bolster its already impressive reach. The company aims to onboard additional brands in the UK, further enhancing its presence and offering diverse payment options to consumers.

Unique Features of Affirm’s Offerings

Affirm’s entry into the UK market is not just about geographical expansion; it also introduces a competitive edge through its unique financing products. The company differentiates itself by providing customers with the flexibility to pay for their purchases over an extended period, offering plans that can stretch up to 36 months. This contrasts sharply with many competitors, who often offer shorter repayment periods.

Here's ads banner inside a post

The products launched in the UK include both interest-free and interest-bearing monthly payment options, calculated on the original principal amount, thus avoiding the pitfalls of increasing or compounding interest. This transparent approach to financing aligns with Affirm’s reputation for prioritizing consumer interests, as Levchin asserts: “We’ve never charged a penny of late fees. We don’t do deferred interest.”

Navigating the Competitive Landscape

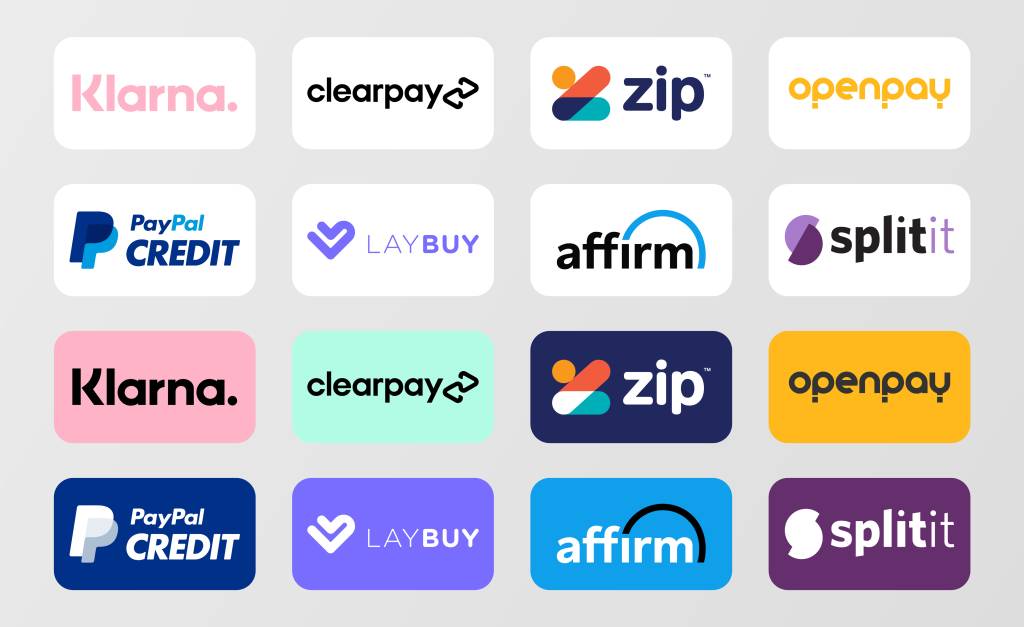

The BNPL sector in the UK is characterized by fierce competition, with established players like Klarna, Block’s Clearpay, Zilch, and PayPal, which entered the BNPL market in 2020. As Affirm seeks to carve out its niche, the firm is not blind to the challenges posed by this competitive landscape. Levchin acknowledges the existing competition but is confident in Affirm’s ability to offer a distinctive value proposition.

“There are lots of competitors here who are doing a sensible job serving the market,” he stated. However, the initial response from merchants during Affirm’s outreach indicated a significant appetite for their services, confirming the potential for successful penetration into the market. This optimism is bolstered by Affirm’s reputation for transparency and customer-centric policies, which resonate well with both consumers and merchants alike.

Moreover, the competitive landscape is not merely a challenge; it also serves as a catalyst for innovation. Affirm’s presence in the UK is likely to prompt existing players to enhance their offerings, potentially leading to better terms for consumers. As more companies vie for market share, improvements in service quality, lower fees, and greater flexibility could emerge as key differentiators, ultimately benefiting consumers.

Regulatory Landscape and Its Implications

Affirm’s UK launch coincides with the government’s ongoing consultation regarding the regulation of the BNPL industry. Proposed regulations aim to ensure clarity for consumers, prevent over-indebtedness, and establish consumer rights in cases of dispute. These discussions underline the importance of responsible lending practices and consumer protection, themes that Affirm is keen to embrace.

“We welcome regulation that is thoughtful,” Levchin remarked, emphasizing the need for frameworks that promote ethical lending while not imposing excessive burdens on consumers. He expressed confidence in Affirm’s capabilities to adapt to regulatory requirements, stating, “We’re very good at automating. We’re very good at writing software. We’ll go do the work.”

This proactive stance on regulation is crucial, especially in an industry that has come under scrutiny for potentially leading consumers into debt traps. By positioning itself as a compliant and consumer-friendly alternative, Affirm is not just addressing current regulatory expectations; it is also laying the groundwork for sustainable growth in a market that may become increasingly regulated.

The Path Ahead for Affirm

The journey ahead for Affirm in the UK is rife with opportunities and challenges. As the company seeks to expand its market share, it must navigate the intricate web of competition while adhering to regulatory expectations. Levchin’s commitment to maintaining a “pristine reputation” in the face of scrutiny reflects Affirm’s long-term vision for sustainable growth.

Furthermore, Affirm’s ability to innovate will be essential as it competes with other fintech companies in the UK. The firm has already hinted at expanding its offerings beyond traditional BNPL services, potentially including features such as budgeting tools or personalized financial advice. By doing so, Affirm can establish deeper relationships with consumers, making it not just a payment provider but a comprehensive financial partner.

As the landscape evolves, so too will Affirm’s strategies. The company’s focus on leveraging data analytics to tailor offerings to consumer needs could provide a significant advantage, helping it to fine-tune its services and improve customer satisfaction. This data-driven approach will be crucial in understanding the preferences of UK consumers, allowing Affirm to remain ahead of the curve.

Impacts on Consumers and Merchants

The expansion of Affirm into the UK market has implications not just for the company but for consumers and merchants as well. For consumers, Affirm’s services provide greater access to credit, particularly for those who may not qualify for traditional financing options. This increased accessibility can empower consumers to make purchases that improve their quality of life, from buying new electronics to financing travel plans.

For merchants, the introduction of Affirm as a payment option can boost conversion rates and average order values. With the flexibility of BNPL options, consumers may be more inclined to make larger purchases, benefiting both the retailer and the consumer. Affirm’s partnerships with various merchants, including travel agencies and retail outlets, highlight the versatility of its offerings and the potential for a win-win situation.

As Affirm navigates this dynamic landscape, its success will hinge on how well it can meet the diverse needs of UK consumers while simultaneously supporting the merchants that partner with it. By focusing on these dual objectives, Affirm is well-positioned to carve out a significant share of the growing BNPL market in the UK.

Looking Forward: The Future of BNPL in the UK

Affirm’s expansion into the UK is a pivotal moment not only for the company but also for the broader BNPL industry. As more players enter the market and regulatory frameworks evolve, the dynamics of consumer finance will undoubtedly shift. The ongoing discussions around responsible lending and consumer protection will shape the future of BNPL services, pushing companies to prioritize ethical practices and transparency.

In this context, Affirm’s approach of prioritizing consumer welfare and responsible lending positions it well to lead by example. As the company grows its footprint in the UK, it will be essential for Affirm to remain adaptable and responsive to both market changes and consumer expectations.

This adaptability will be crucial as consumers become increasingly savvy and demanding about their financial products. The UK market, with its diverse consumer base and evolving needs, represents both a challenge and an opportunity for Affirm. How the company leverages this opportunity could set the tone for its future expansions into other international markets, ultimately defining its legacy in the global fintech landscape.

As Affirm embarks on this exciting new chapter, all eyes will be on its performance in the UK and how it navigates the complexities of competition, regulation, and consumer expectations. The outcomes of these endeavors could significantly influence the direction of the BNPL industry as a whole, making Affirm’s UK launch a key moment to watch in the coming months.